Slide 1 of 21

Slide 1 - Chapter 12: Partnership Operations

Chapter 12: Partnership Operations

Division of Profits and Losses under Philippine Civil Code

---

Photo by Iñaki del Olmo on Unsplash

Generated from prompt:

Create a comprehensive presentation titled "Chapter 12: Partnership Operations" based entirely on the uploaded document "Partnership Operations.pdf" (15 pages). Structure: 1. Title Slide – Chapter 12: Partnership Operations 2. Learning Objectives (as shown on page 1) 3. Concept Overview – Division of Profits and Losses - Rules under Art. 1797 of the Philippine Civil Code - Industrial vs Capitalist Partner definitions 4. Partnership Agreements – Key Provisions - Salaries - Bonuses - Interest on Capital Contributions - Order of Allocation Include ALL Illustrations exactly as shown in the document. For each Illustration (1 to 9): - Create separate slides per case (Case 1, Case 2, etc.) - Snip and insert the original illustration tables/calculation layouts as images for clarity (use the scanned visuals per page). - Add a short discussion slide before each illustration explaining the concept involved. Illustrations to include: - Illustration 1: Salaries (Case 1 and Case 2) - Illustration 2: No P/L Ratio - Illustration 3: Bonus (Profit and Loss cases) - Illustration 4: Bonus with limit - Illustration 5: Interest on Capital (weighted average computation) - Illustration 6: Profit after salaries (salaries recognized as expenses) - Illustration 7: Reconstruction of information (T-account squeeze method) - Illustration 8: Reconstruction (Pro forma method) - Illustration 9: P/L ratio in fractions End with: - Chapter Summary (page 15 content) Ensure calculations and tables match the document exactly. Keep layout clean and academic. Use clear section dividers for each Illustration.

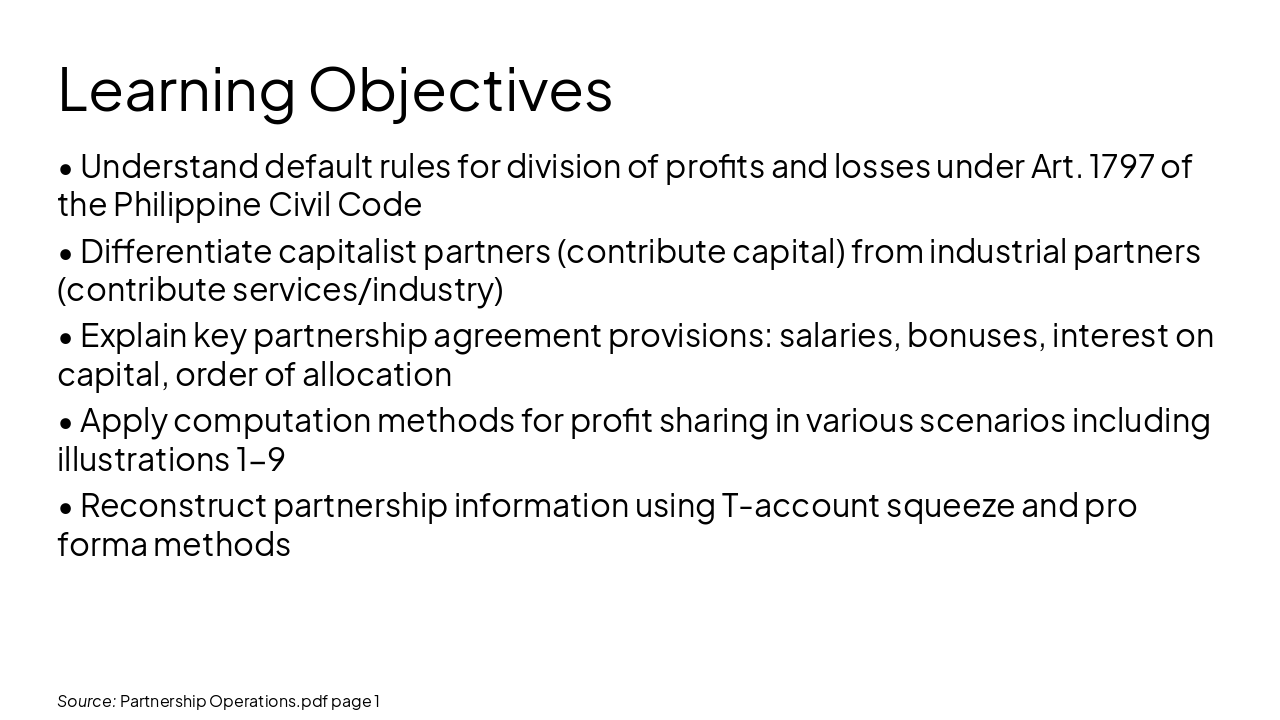

Explore default rules for profit/loss division under Art. 1797, capitalist vs. industrial partners, key agreements (salaries, bonuses, interest), allocation order, and practical illustrations (1-9) with T-account reconstruction for accounting mastery

Chapter 12: Partnership Operations

Division of Profits and Losses under Philippine Civil Code

---

Photo by Iñaki del Olmo on Unsplash

Source: Partnership Operations.pdf page 1

1

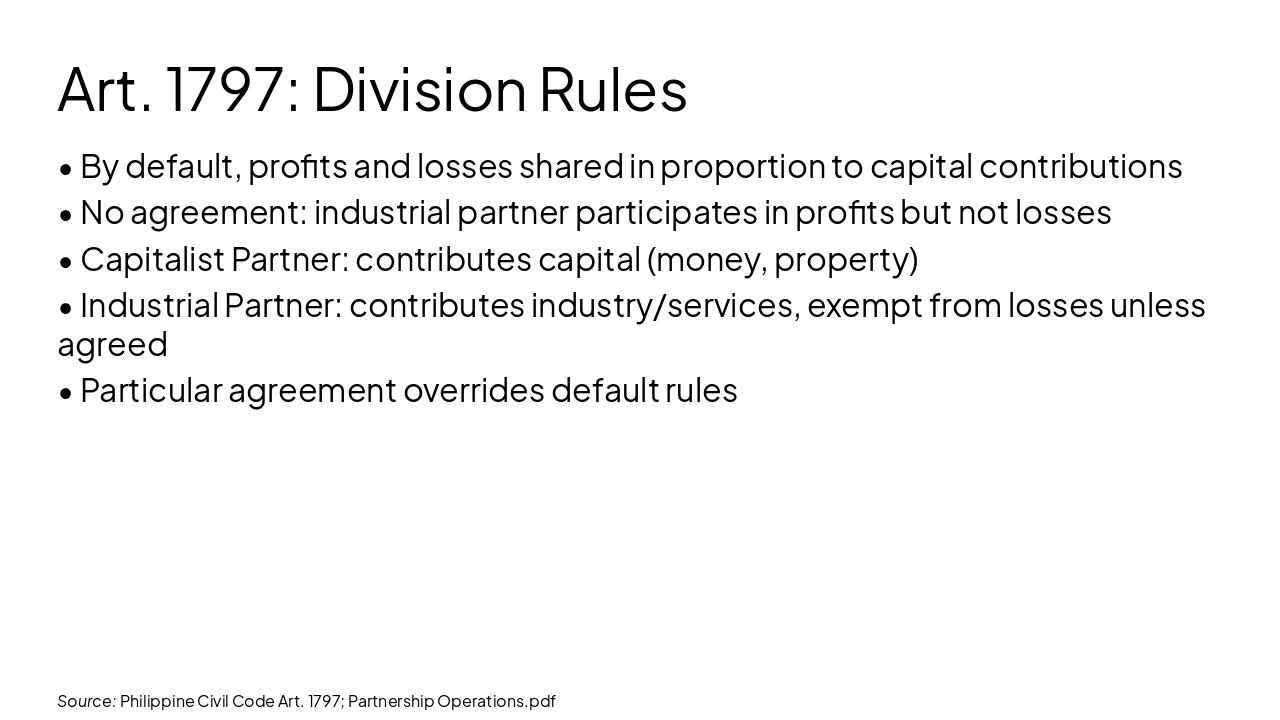

Concept Overview - Rules under Art. 1797 Philippine Civil Code

---

Photo by Logan Voss on Unsplash

Source: Philippine Civil Code Art. 1797; Partnership Operations.pdf

2

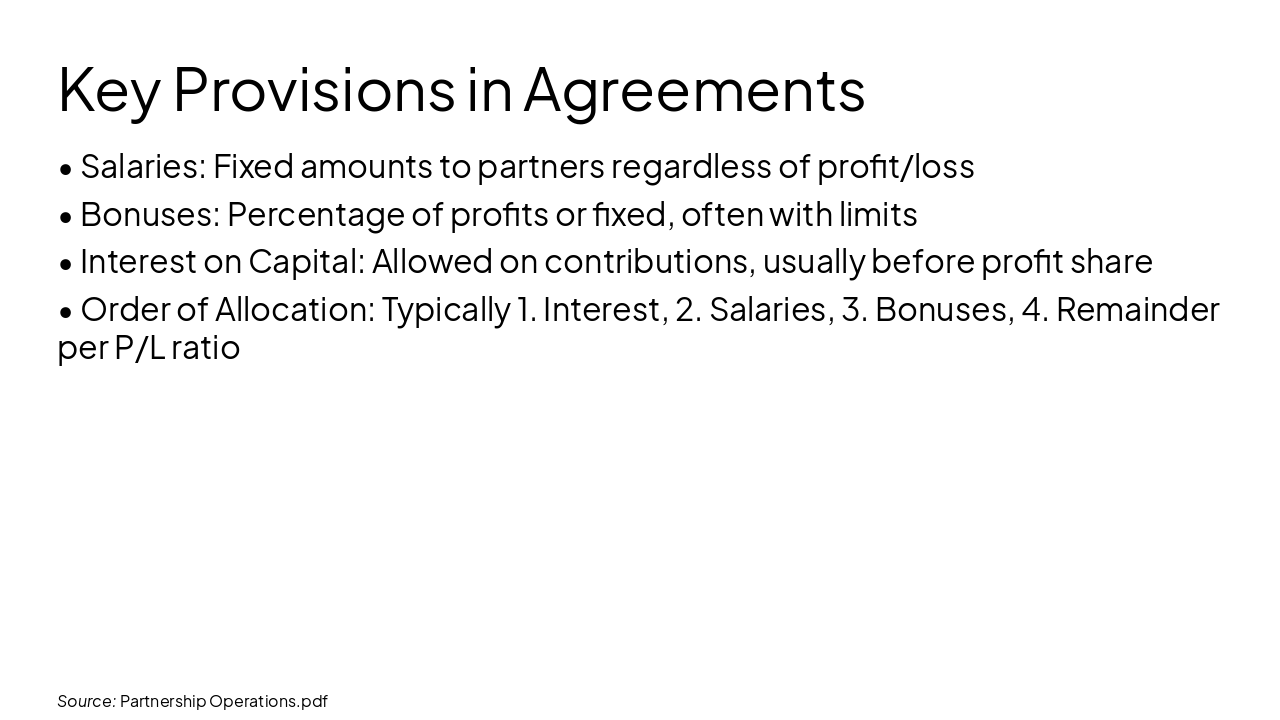

Key Provisions: Salaries, Bonuses, Interest, Allocation Order

---

Photo by Cytonn Photography on Unsplash

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

| Partner | Capital | Ratio | Salary | Case 1 Profit 40,000 (Share) | Case 2 Profit 20,000 (Share) |

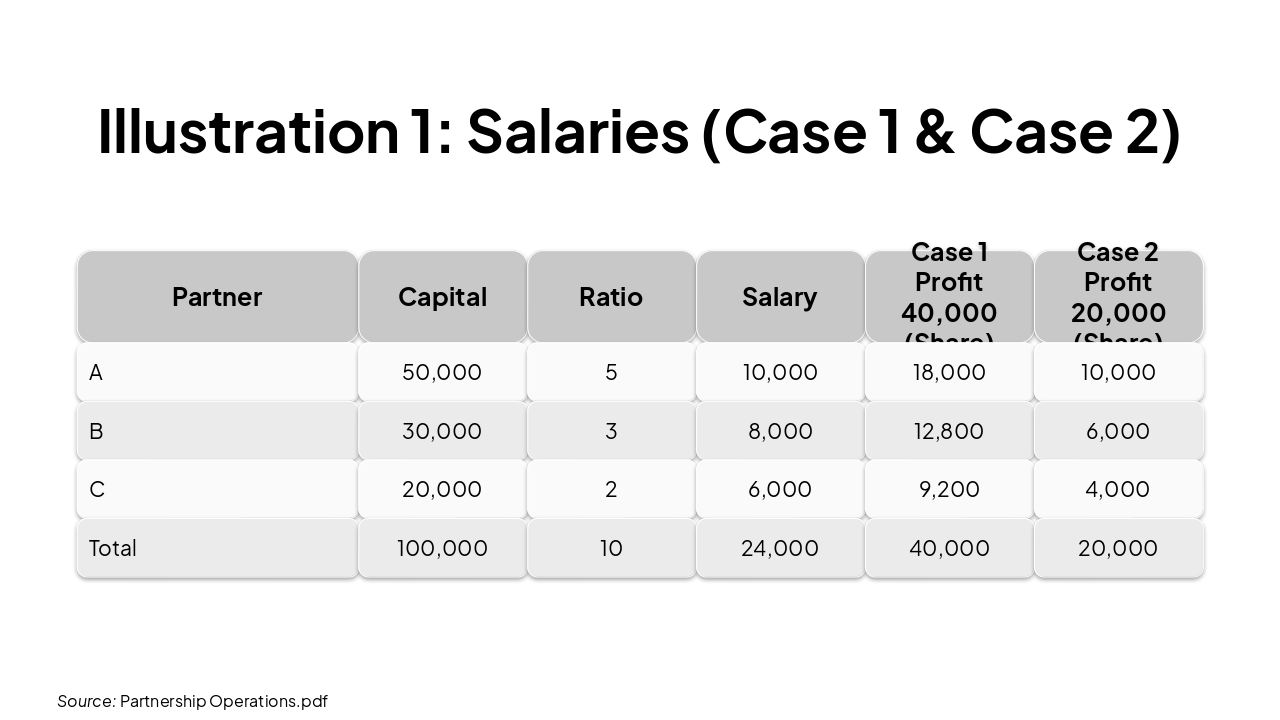

|---|---|---|---|---|---|

| A | 50,000 | 5 | 10,000 | 18,000 | 10,000 |

| B | 30,000 | 3 | 8,000 | 12,800 | 6,000 |

| C | 20,000 | 2 | 6,000 | 9,200 | 4,000 |

| Total | 100,000 | 10 | 24,000 | 40,000 | 20,000 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

| Partner | Capital | Ratio | Profit 20,000 Share |

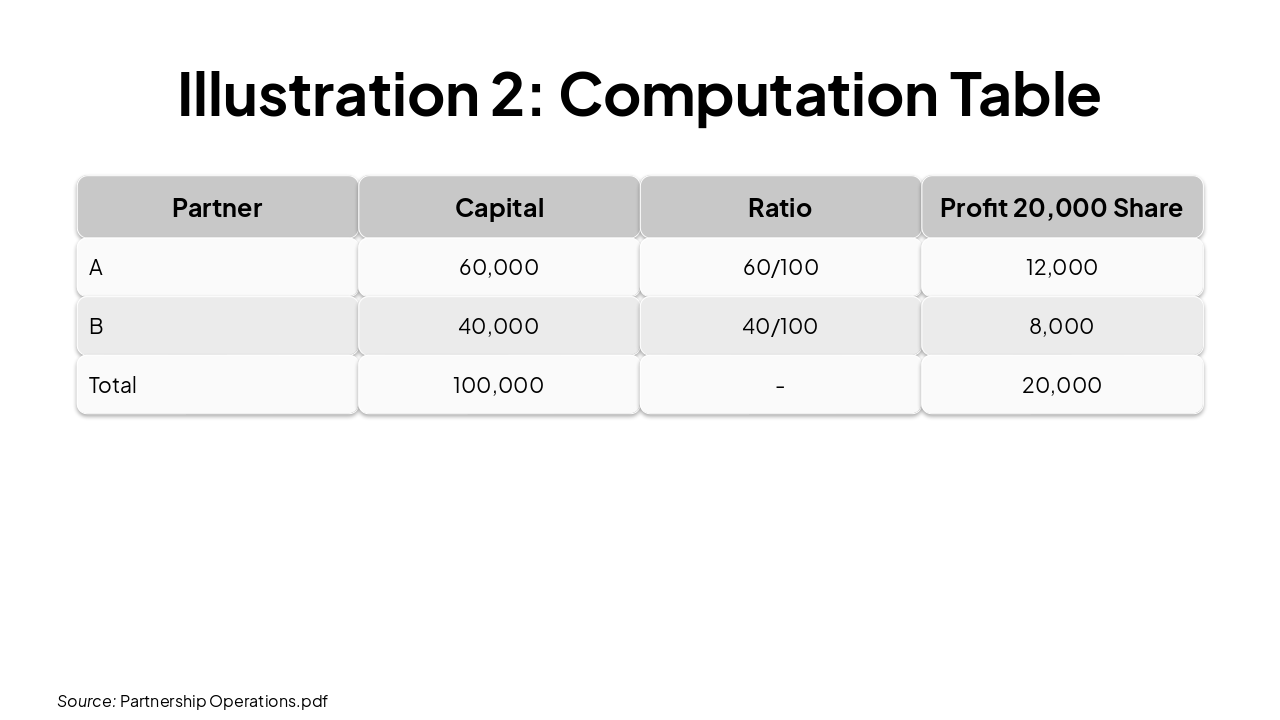

|---|---|---|---|

| A | 60,000 | 60/100 | 12,000 |

| B | 40,000 | 40/100 | 8,000 |

| Total | 100,000 | - | 20,000 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

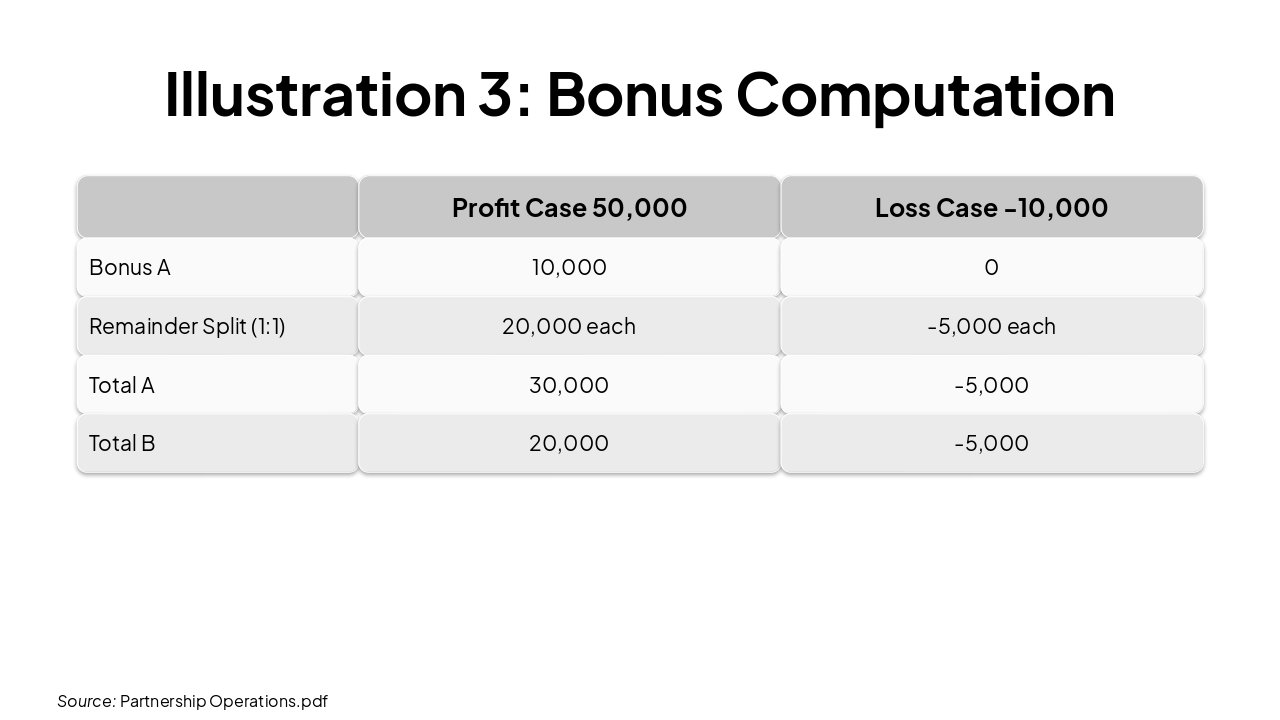

| Profit Case 50,000 | Loss Case -10,000 | |

|---|---|---|

| Bonus A | 10,000 | 0 |

| Remainder Split (1:1) | 20,000 each | -5,000 each |

| Total A | 30,000 | -5,000 |

| Total B | 20,000 | -5,000 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

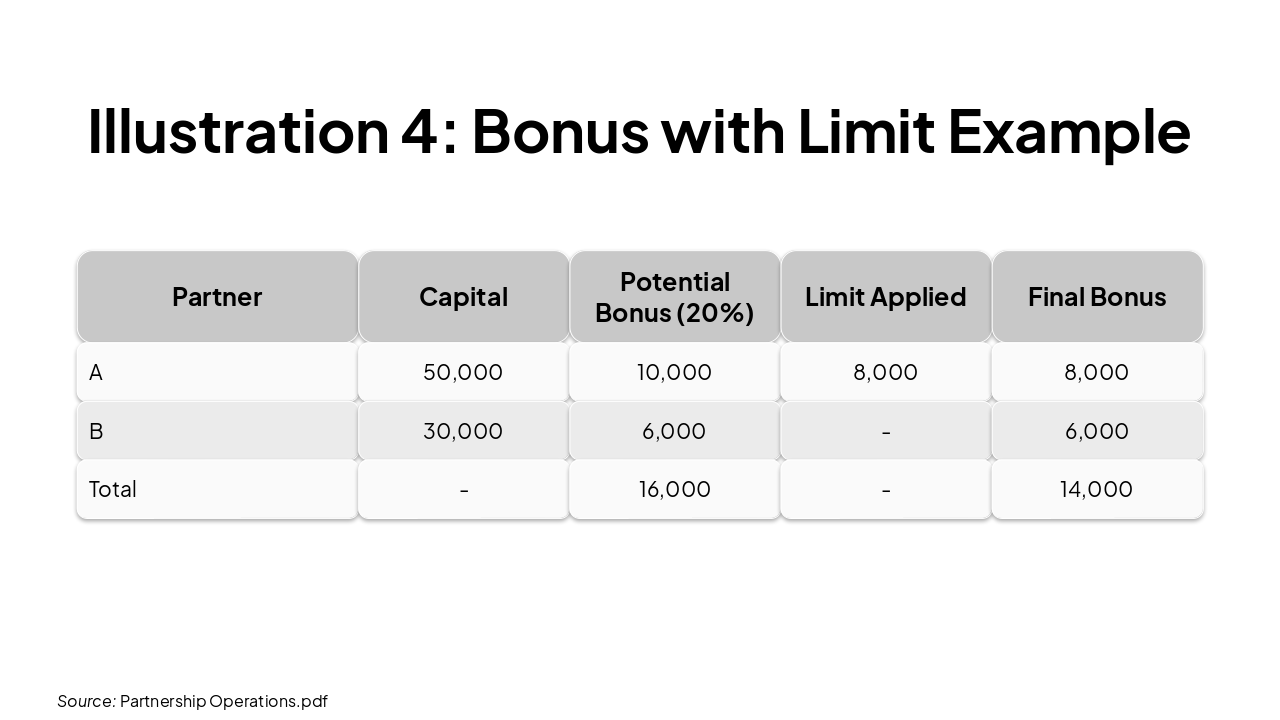

| Partner | Capital | Potential Bonus (20%) | Limit Applied | Final Bonus |

|---|---|---|---|---|

| A | 50,000 | 10,000 | 8,000 | 8,000 |

| B | 30,000 | 6,000 | - | 6,000 |

| Total | - | 16,000 | - | 14,000 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

| Partner | Beg Cap | Additions | Drawings | Avg Cap | Interest 12% |

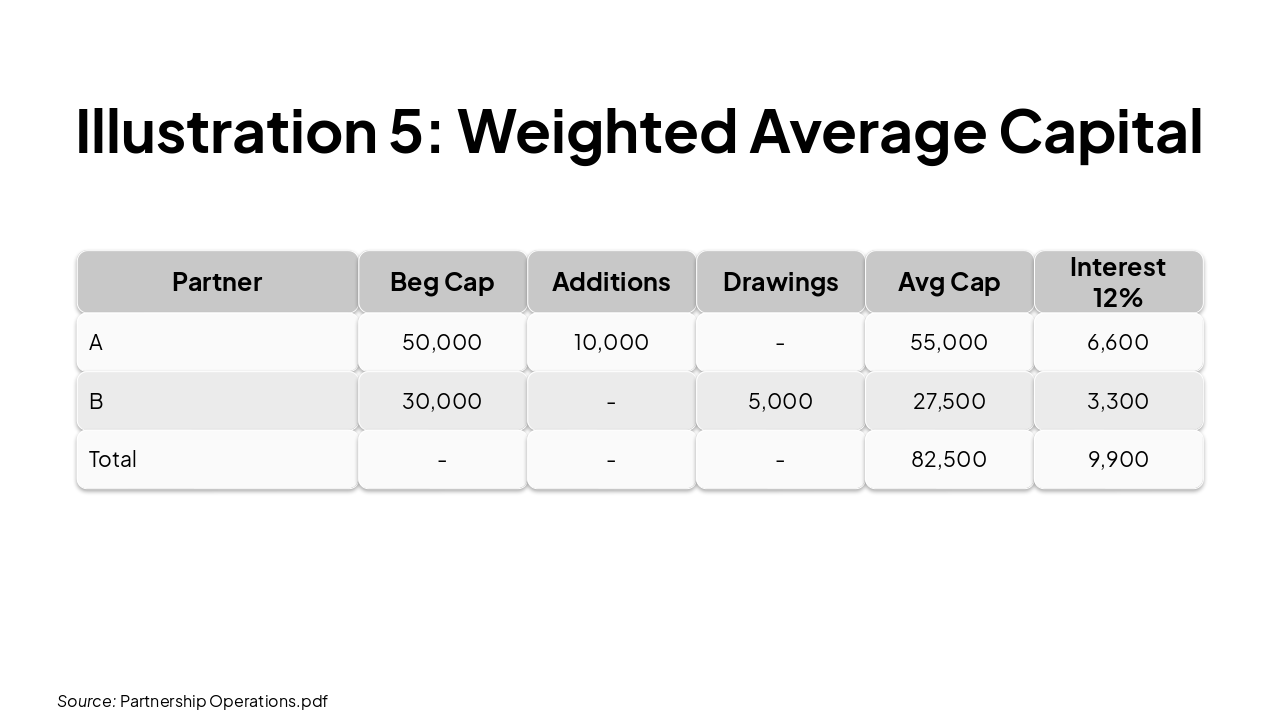

|---|---|---|---|---|---|

| A | 50,000 | 10,000 | - | 55,000 | 6,600 |

| B | 30,000 | - | 5,000 | 27,500 | 3,300 |

| Total | - | - | - | 82,500 | 9,900 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

| Salaries | Remainder (Ratio 5:3:2) | Total Share | |

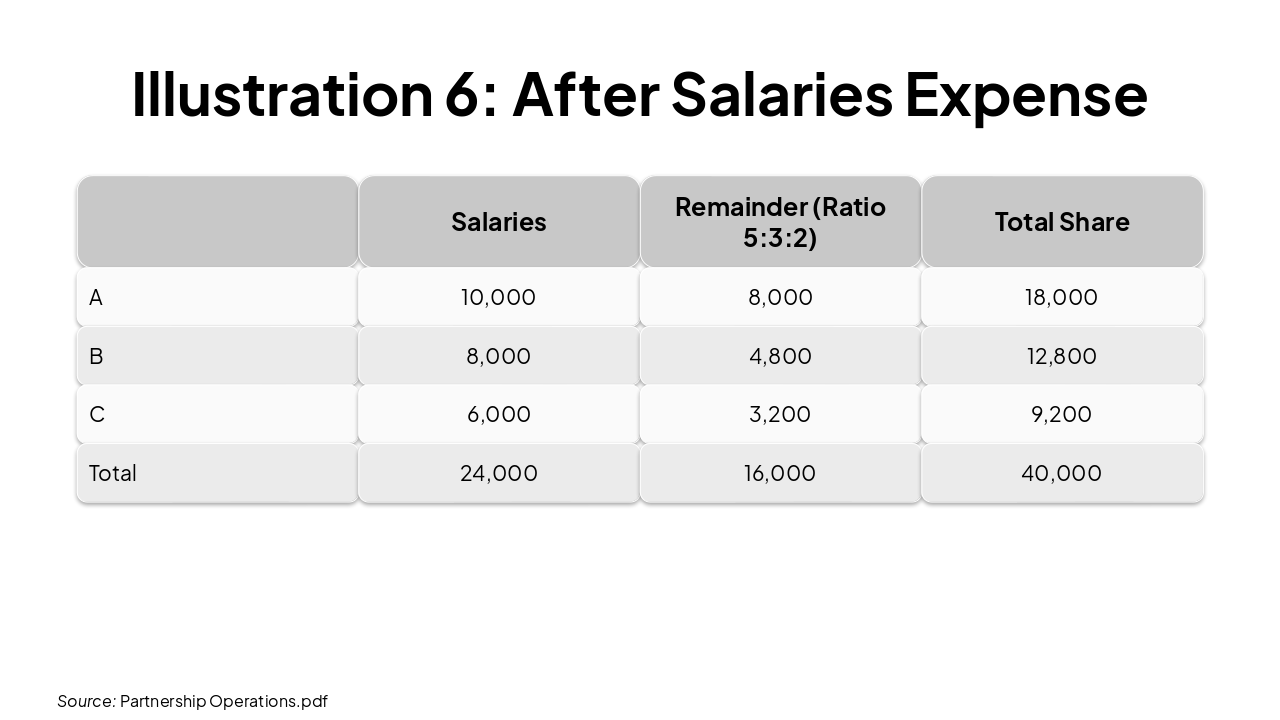

|---|---|---|---|

| A | 10,000 | 8,000 | 18,000 |

| B | 8,000 | 4,800 | 12,800 |

| C | 6,000 | 3,200 | 9,200 |

| Total | 24,000 | 16,000 | 40,000 |

Source: Partnership Operations.pdf

Source: Partnership Operations.pdf

---

Photo by FIN on Unsplash

Source: Partnership Operations.pdf

Key Takeaways:

Master partnership profit sharing for accounting accuracy

---

Photo by Erik Mclean on Unsplash

Explore thousands of AI-generated presentations for inspiration

Generate professional presentations in seconds with Karaf's AI. Customize this presentation or start from scratch.