Slide 1 of 20

Slide 1 - Chapter 12: Partnership Operations

Chapter 12: Partnership Operations

Division of Profits and Losses Under Philippine Civil Code

---

Photo by Iñaki del Olmo on Unsplash

Generated from prompt:

Create a comprehensive presentation titled "Chapter 12: Partnership Operations" based entirely on the uploaded document "Partnership Operations.pdf" (15 pages). Structure: 1. Title Slide – Chapter 12: Partnership Operations 2. Learning Objectives (as shown on page 1) 3. Concept Overview – Division of Profits and Losses - Rules under Art. 1797 of the Philippine Civil Code - Industrial vs Capitalist Partner definitions 4. Partnership Agreements – Key Provisions - Salaries - Bonuses - Interest on Capital Contributions - Order of Allocation Include ALL Illustrations exactly as shown in the document. For each Illustration (1 to 9): - Create separate slides per case (Case 1, Case 2, etc.) - Snip and insert the original illustration tables/calculation layouts as images for clarity (use the scanned visuals per page). - Add a short discussion slide before each illustration explaining the concept involved. Illustrations to include: - Illustration 1: Salaries (Case 1 and Case 2) - Illustration 2: No P/L Ratio - Illustration 3: Bonus (Profit and Loss cases) - Illustration 4: Bonus with limit - Illustration 5: Interest on Capital (weighted average computation) - Illustration 6: Profit after salaries (salaries recognized as expenses) - Illustration 7: Reconstruction of information (T-account squeeze method) - Illustration 8: Reconstruction (Pro forma method) - Illustration 9: P/L ratio in fractions End with: - Chapter Summary (page 15 content) Ensure calculations and tables match the document exactly. Keep layout clean and academic. Use clear section dividers for each Illustration.

This chapter explores division of profits and losses in partnerships under Philippine Civil Code Art. 1797. Covers default rules, industrial vs. capitalist partners, key agreement provisions (salaries, bonuses, interest on capital, allocation order),

Chapter 12: Partnership Operations

Division of Profits and Losses Under Philippine Civil Code

---

Photo by Iñaki del Olmo on Unsplash

---

Photo by Alvaro Reyes on Unsplash

1

Key goals for understanding partnership operations

---

Photo by Dom Fou on Unsplash

2

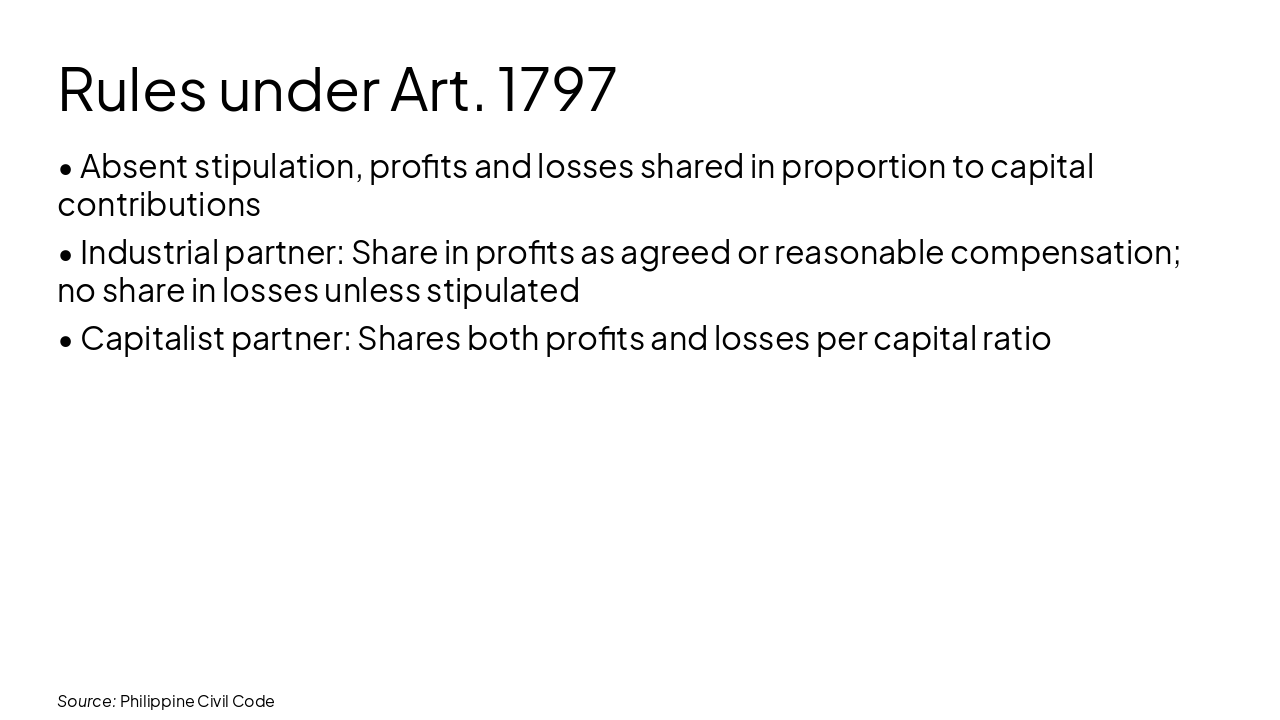

Rules under Philippine Civil Code

Source: Philippine Civil Code

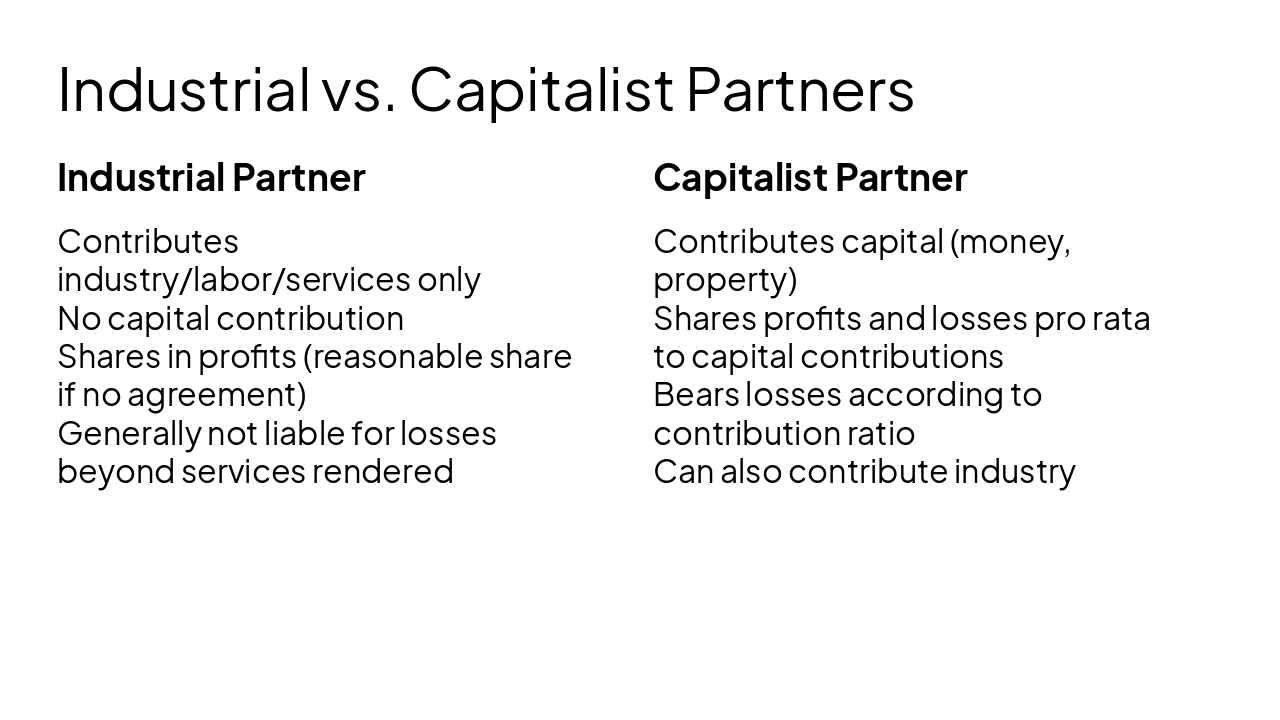

Industrial Partner Contributes industry/labor/services only No capital contribution Shares in profits (reasonable share if no agreement) Generally not liable for losses beyond services rendered

Capitalist Partner Contributes capital (money, property) Shares profits and losses pro rata to capital contributions Bears losses according to contribution ratio Can also contribute industry

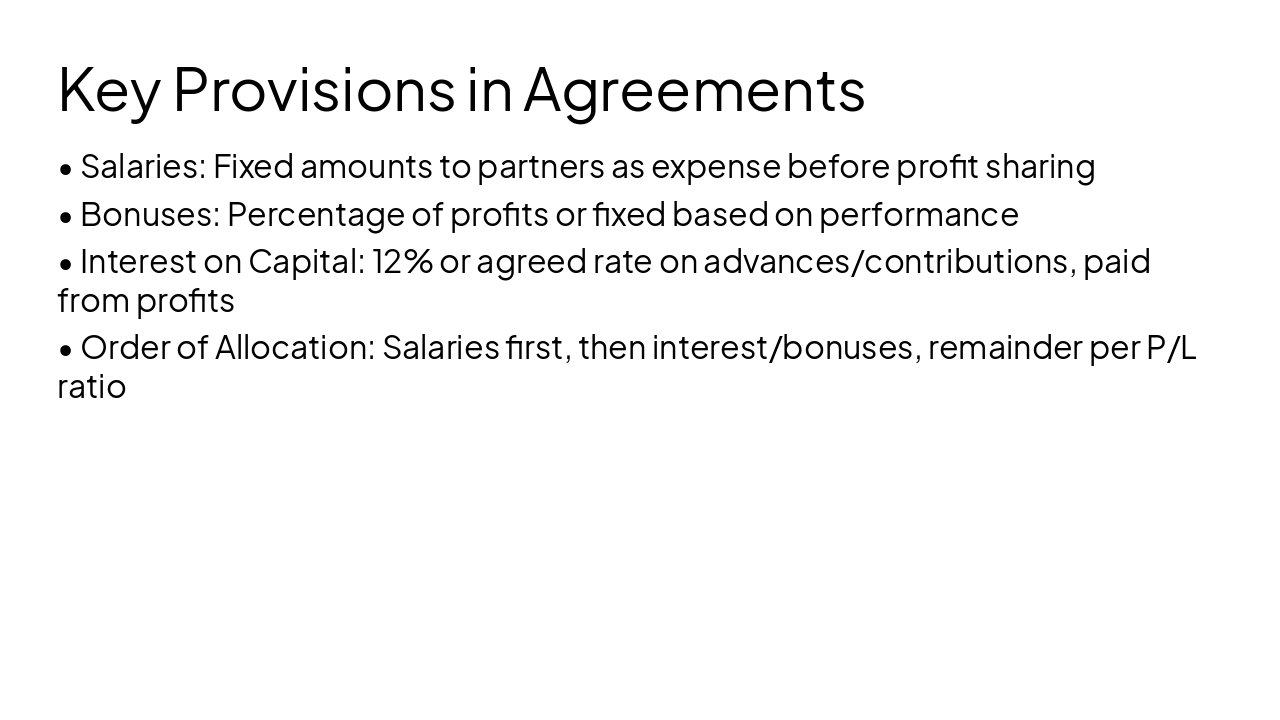

Salaries paid first as expenses before dividing remainder per agreement or default rules

---

Photo by Blake Wisz on Unsplash

Default equal sharing of profits when no ratio specified

---

Photo by Arturo Añez on Unsplash

Bonuses allocated before remainder profit sharing; losses absorb bonuses if insufficient profit

Bonus capped at certain amount or percentage to protect other partners

---

Photo by Adam Śmigielski on Unsplash

---

Photo by Charles Forerunner on Unsplash

Weighted average capital for interest computation

---

Photo by rc.xyz NFT gallery on Unsplash

Explore thousands of AI-generated presentations for inspiration

Generate professional presentations in seconds with Karaf's AI. Customize this presentation or start from scratch.